PARKONOMICS

A Deep Dive Series on the Economics of Parking

By Andrew Sachs, CAPP

On February 23, 2026, Uber Technologies announced an agreement to acquire SpotHero, the leading parking reservation platform in North America. SpotHero operates a network of more than 13,000 garages, lots, and valets across over 400 cities and has facilitated more than $2 billion in lifetime parking reservations since its founding in 2011.

Uber CEO Dara Khosrowshahi framed the deal as a convenience play: helping drivers find parking through the Uber app. That framing is accurate as far as it goes. But for those of us who own and operate parking assets, it dramatically understates what is actually happening.

This acquisition is about Uber purchasing the physical infrastructure layer it needs to compete in an autonomous future.

Why Uber needs parking

Uber’s single largest expense is driver payments — $18.6 billion in Q1 2025 alone. The company’s entire business model sits on top of human labor. If that labor can be replaced by autonomous vehicle (AV) technology that competitors like Waymo own outright, Uber’s role as middleman becomes unnecessary.

This is not hypothetical. During Uber’s Q2 2025 earnings call, Khosrowshahi admitted that Waymo robotaxis operating on the Uber platform in Austin, Texas, and Atlanta were more productive than 99% of Uber’s human drivers. Meanwhile, Waymo has surpassed Lyft in gross bookings in San Francisco and is launching new markets — Dallas, London, Denver, and Miami — without Uber’s partnership.

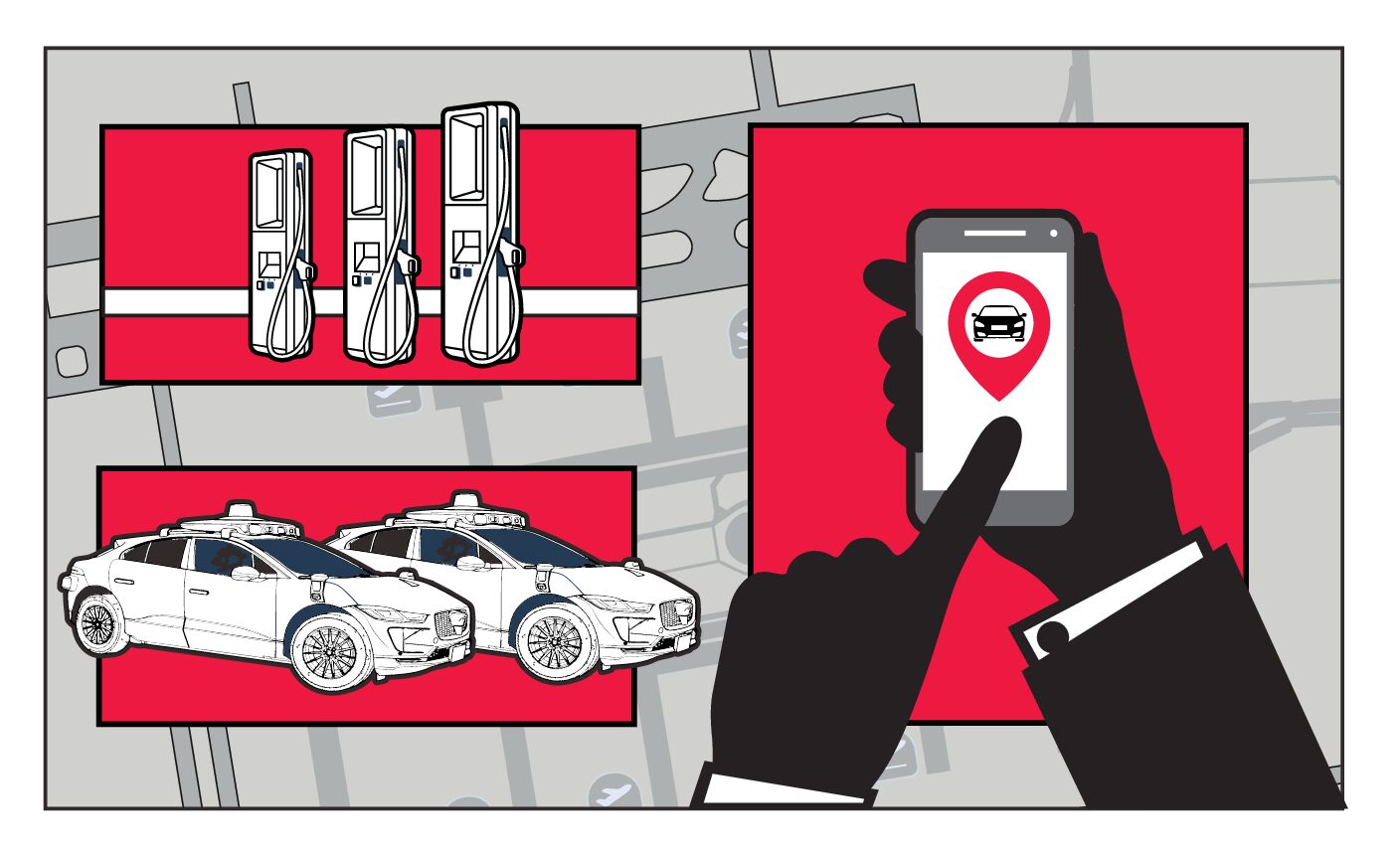

Uber has responded with a fundamental strategic pivot: more than $600 million invested in the electric vehicle (EV) manufacturer Lucid Group and the AV technology developer Nuro, Inc., plans to purchase more than 20,000 vehicles, and a partnership with Nvidia targeting 100,000 AVs. At the technology tradeshow CES 2026, held this past January in Las Vegas, the three companies unveiled a production-intent robotaxi — the Lucid Gravity SUV powered by Nuro’s autonomous driving system and NVIDIA’s DRIVE AGX Thor computing platform. The first deployments are planned for San Francisco in late 2026, directly on Waymo’s home turf.

Autonomous vehicles do not just drive. Between trips, they need to stage, charge, undergo maintenance, and rotate between deployment zones. Industry data shows roughly 50% of rideshare vehicle miles are driven without a passenger. Strategically positioned staging facilities reduce that deadheading, and SpotHero’s network of 13,000+ connected locations, with 500+ already outfitted for AV entry and exit, is exactly that infrastructure.

What this means for your operation

The opportunity

Parking operators working with SpotHero will gain access to Uber’s massive consumer base and its network of vehicle charging and fleet partners. For an industry that remains remarkably fragmented, this represents a significant acceleration of digital transformation.

SpotHero’s IQ dynamic pricing platform has increased operator revenue by up to 15%. Its latest iteration, Precision Pricing, delivers more than 4,000 rate recommendations per week. Layering Uber’s demand data and event forecasting on top of that engine could meaningfully improve yield management.

The longer-term opportunity is even more compelling. As autonomous fleets scale, facilities equipped for AV staging, charging, and servicing will command premium economics. This is the future-proofing thesis that our Parkonomics column has articulated from the beginning: The first floor of a parking garage is not just a parking level. It is an extension of the curb, capable of absorbing rideshare pickups, delivery logistics, and autonomous fleet operations.

The risk

Those of us who have watched how Uber manages its relationships with human drivers should be clear-eyed about the platform dynamics at play. Once Uber controls the dominant digital booking layer for parking, it gains enormous leverage over pricing and commission structures.

Uber’s history is instructive. The company used investor subsidies to build an indispensable network, then gradually adjusted terms in its favor as participants became dependent. There is no structural reason this pattern could not repeat in parking.

The parking industry’s fragmentation makes individual operators particularly vulnerable to this kind of aggregator power. Independent operators lack the scale to negotiate favorable terms, and switching costs rise as facilities become more deeply integrated into Uber’s commercial ecosystem.

Getting ready: the practical checklist

For operators evaluating their position, the Uber-SpotHero deal makes several strategic imperatives urgent:

Diversify your digital channels. Do not become exclusively dependent on any single booking platform. Maintain direct consumer relationships through your own website, app, and loyalty programs. Think of the hotel industry’s experience with online travel agencies as a cautionary tale.

Own your SEO and online presence. If Uber becomes the primary way consumers find your facility, you’ve ceded control of your customer relationship. Invest in your own digital discoverability.

Evaluate your physical infrastructure. Flat floors, adequate ceiling clearance, robust electrical capacity, and connected access control systems are the prerequisites for serving autonomous fleets. Facilities that can support EV charging at scale, starting with 20 stations but with conduit capacity for 100 or more, will capture outsized value.

Invest in data connectivity. License plate recognition, IoT sensors, and vehicle-to-everything (V2X) communication infrastructure are becoming table stakes. SpotHero’s HeroConnect platform already enables vehicles to autonomously find, book, enter, pay for, and exit facilities. Your infrastructure needs to speak this language.

Negotiate early and carefully. The terms Uber offers operators in the first year will be the most generous. Pay close attention to commission structures, data ownership clauses, and exclusivity provisions.

The bottom line

Uber didn’t buy a parking app. It bought physical infrastructure for an autonomous future. The parking industry’s $100 billion market is poised for a fundamental shift from passive vehicle storage to active mobility infrastructure. Operators who position their assets for this transition will capture outsized value. Those who don’t will find themselves holding depreciating assets in a world that has moved on.

The prudent response is not to refuse to engage; that ship has sailed. It is to participate in the Uber ecosystem while ensuring your operation is never exclusively dependent on it. Diversify your channels, own your customer relationships, and build the physical infrastructure that autonomous fleets will need. The next 18 months will determine who is ready.

Andrew Sachs, CAPP, is an entrepreneur and venture capital investor with deep roots in commercial real estate and parking operations, owning Harbor Park Garage in Baltimore’s Inner Harbor and leading Gateway Parking Services. He can be reached at [email protected].